Paying for College: Federal Student Aid Programs

Every year, more than $120 billion is available in federal student aid through grants, work-study, and loans.

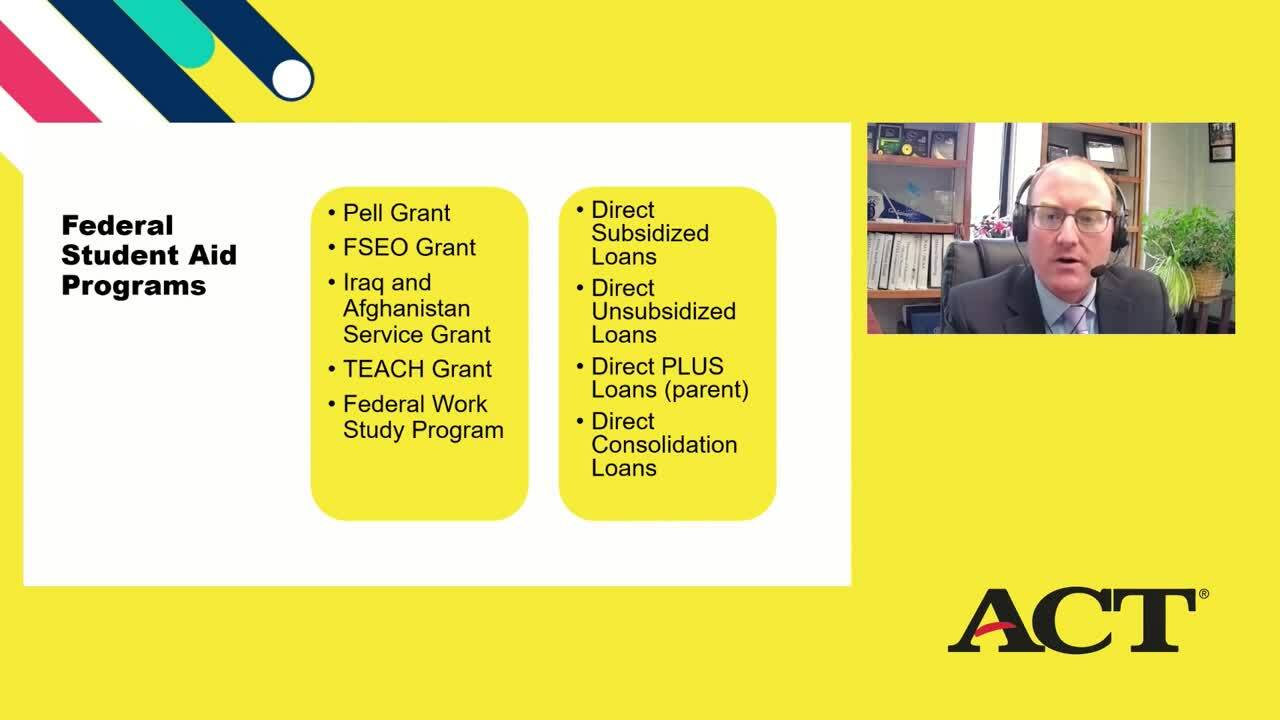

Federal Student Grant Program

Below are the major grant programs available through the federal government. Grants are considered “free money” and do not need to be repaid.

- Federal Pell Grant: The Pell Grant program is the largest federal grant program available to students. These grants are awarded based on financial need. The money may be used toward tuition, room and board, books, or other educational costs.

- Federal Supplemental Educational Opportunity Grant (FSEOG): These grants are provided to a limited number of undergraduates based on the significance of their financial need.

- Teacher Education Assistance for College and Higher Education (TEACH) Grant: These grants are for students who plan to teach in a high-need field at the elementary or secondary level. Students must agree to serve for a minimum of four-years as a full-time teacher that serves low-income students. If a recipient does not complete the service requirements, the grant will be converted to a loan that must be repaid.

- Iraq and Afghanistan Service Grant: These grants are for students whose parent or guardian was a member of the U.S. armed forces and died as a result of performing military service in Iraq or Afghanistan after 9/11. There are additional financial need and age qualifications.

Navigating the Financial Aid Process

Federal Student Loan Program

The US Department of Education offers loans to eligible students to help cover educational costs at a four-year college or university, community college, or trade, career, or technical school. Below are the major loan programs available through the federal government. Loans are borrowed funds that you must repay with interest.

- Direct Subsidized Loans: These loans are available to undergraduate students with financial need. The US Department of Education pays the interest for your loan while you are enrolled at least half-time, for the first six months after you leave school, and during periods of deferment (a suspension of payment allowed under certain conditions).

- Direct Unsubsidized Loans: These loans are available to undergraduate and graduate students–with no requirement to demonstrate financial need. For unsubsidized loans, you are responsible for paying the interest at all times. If you choose not to pay the interest while you are in school, the interest will accrue and be added to the loan – which means your loan balance will continue to grow while you are enrolled.

- Direct PLUS Loans: These loans are available to the parents of dependent students and are intended to cover the difference between the cost of attendance and all other financial aid. Financial need is not required. Parent borrowers are expected to begin repayment after the loan is fully dispersed, but may choose to defer payments while students are in school. In this case, interest will accrue and be capitalized.

Federal Work-Study

A Federal Work-Study program provides part-time employment for eligible students in exchange for funds intended for educational expenses. Jobs should be related to your program of study and the amount you earn cannot exceed your total Federal Work-Study award. The program is coordinated through financial aid offices at participating colleges and universities. Each school will have its own process for job placements and may be limited to a first-come, first-served basis.

Learn More About Paying for College

ACT provides comprehensive college planning resources to help you make informed decisions about your educational and professional path. Explore our paying for college resources to gain valuable insights on financial aid, scholarship tips and much more!